- Intellego Newsletter

- Posts

- Applied Budgeting

Control your money, don’t let it control you.

🎼 📖 Read Intellego #020 by listening to:

Money is often a source of fear, stress, and anger. Financial problems are one of the major causes of divorce, breaking relationships and ruined families. But it does not need to be this way.

What if money brings you joy instead of frustration? It’s the solution, not the problem? What if money was on your side?

Money impacts many aspects of our lives, so give the proper attention to it. Not less, not more. Be the master of money, not its servant.

Create systems to simplify your life. Exercising and budgeting are good examples of systems you can build. Take responsibility for your health, financial situation and future.

Don’t let weeks, months and years pass by you idle. Take action, own it, decide, evaluate strategies, learn, readjust course, seek progress, achieve goals and celebrate them.

If you’re lucky enough, you will live approximately four thousand weeks. Reclaim time, don’t miss the bus. We all have a limited window of opportunity in front of us called now.

Today I want to tell you an inspiring story based on a true facts.

Sarah is a dedicated chief nurse. A 33-year-old woman, single mom with two kids living in Brazil.

She navigates the bustling corridors of two different hospitals across alternating shifts. I dare to say her work routine is a living testament of commitment and responsibility.

In one hospital, she leads a team of eager junior nurses, mentoring them through the intricacies of emergency care.

While in the other, she is involved in the critical care unit, handling cases that demand high levels of expertise and emotional resilience.

Despite the physical and mental toll of her demanding schedule, Sarah decided to work multiple shifts to secure a stable financial future for her and her family.

This includes her children’s education and her own dream of reducing her working hours in the future.

Her plan is to focus more on specialized patient care and increase family time. That’s far beyond money. A valid goal in my view.

“Whether you think you can, or you think you can't. You're right.”

Henry Ford

Details

Life is short. Spend it wisely.

Know your numbers. Sarah reviews her goals and budget in her scarce time, applying a disciplined 60-20-20 rule to her finances.

She’s tried different budget rules in the past, but this hybrid model suited best her overall needs.

She does not face budgeting as a survival tool or a burden. In fact, it helps her to better allocate the money she disposes to meet her needs, wants, and plans.

Here is an x-ray of Sarah’s current budget:

60% for needs: it covers the essentials—mortgage, utilities, groceries, and transportation, ensuring her family’s comfort and stability.

20% for wants: it allows Sarah to relax with her family. Perhaps a weekend movie or a modest vacation, keeping life’s joys accessible amidst her busy schedule.

20% for savings: she directs towards savings and debt repayment. Her goal is to lessen her workload without compromising her financial security.

Balancing life across two hospitals, Sarah’s story is a compelling narrative of resilience and discipline.

Her example reflects the realities faced by many people in different industries and countries, who often stretch their limits in pursuit of both professional fulfillment and financial stability.

Fear, uncertainty, anxiety. We don’t know when the next financial bubble will burst.

To fight Murphy, create your financial safety net. Get yourself prepared for the rainy days because they will come, regardless if you like them or not.

Effective budget management is crucial in today’s financial climate, especially for those professionals who often balance demanding work schedules with personal financial goals.

You don’t let your car run out of gas in the middle of a highway, right? I assume you don’t want that kind of trouble and stress into your life.

A sustainable budget is not just about tracking expenses or cutting back. It’s about understanding and implementing a plan that aligns with your income, lifestyle, and financial objectives. It gives you peace of mind.

“Don’t let making a living prevent you from making a life.”

John Wooden

Rule Explained

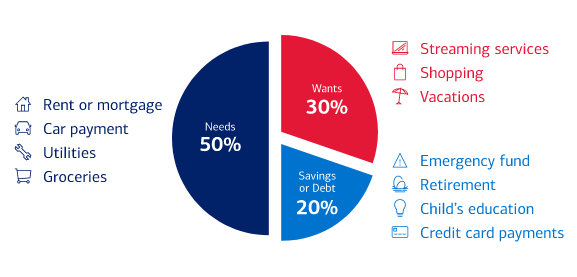

The 50-30-20 rule is a popular budgeting technique. It divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment.

This method provides a clear financial structure. It’s simple and effective, but maybe too radical for beginners.

For a nurse making R$6,300 per month, the 50-30-20 distribution would look like this:

Needs (50%): R$3,150 - This would cover essentials such as housing, utilities, groceries, transportation, insurance, basic healthcare and medications.

Wants (30%): R$1,890 - This portion includes non-essential expenditures like dining out, entertainment, leisure activities, vacations, and personal shopping.

Savings and Debt Repayment (20%): R$1,260 - This amount covers savings, retirement, investments, emergency funds, and paying off debts.

Actual Budget

Sarah earns R$6,300 monthly. Her current budget might not perfectly align with the 50-30-20 rule because of various personal and professional factors.

Here’s her actual budget break down:

Housing and utilities (R$2,000) - Living in a major city, housing costs can be quite high.

Transportation (R$300) - This includes car payments and fuel or public transport tickets.

Groceries (R$600) - Reflects a reasonable amount for a nutritious diet.

Insurance and healthcare (R$300) - Includes health insurance and out-of-pocket medical expenses.

Education and professional development (R$500) - Crucial for maintaining nursing credentials and ongoing education.

Entertainment and dining out (R$600)

Miscellaneous (R$700) - Clothing, gifts, and other personal expenses.

Savings and investments (R$1,300) - Slightly above the 20% recommended, which is positive.

Sarah’s actual budget deviates from the 50-30-20 rule in the needs category, consuming 60% of her income rather than the recommended 50%.

Her wants are under control at about 19%, and her savings exceed the guideline, which is beneficial if sustainable.

"He who buys what he does not need, steals from himself.”

Swedish Proverb

Hybrid Model

Money is a mirror. It’s a reflection of who you're within.

Consider the specific needs and challenges that any person may face during a lifetime. Irregular shifts, variable incomes, career changes, healthcare bills, emergencies and continuous professional development.

A more tailored budgeting approach could be more practical. The hybrid model suggested here divides income into three categories: 60% for needs, 20% for wants, and 20% for savings and debt repayment.

For Sarah, the hybrid budget model would look like this:

Needs (60%): R$3,780 - This amount comfortably covers all her essentials, ensuring she doesn’t have to worry about her basic monthly obligations.

Wants (20%): R$1,260 - This reduction from the more traditional 30% allows Sarah to still enjoy life’s pleasures but with a moderate cap, ensuring she doesn’t overspend in this category.

Savings and Debt Repayment (20%): R$1,260 - Increasing this allocation helps Sarah achieve her financial goals quicker, whether that’s paying off debt or saving for a future investment like a home or further education.

This division reflects her current lifestyle, but it can be adjusted anytime.

Conclusion

While the 50-30-20 rule provides a sound foundation for budgeting, it doesn’t fit everyone’s unique circumstances.

Sarah’s situation illustrates how a hybrid model can offer a more customized and realistic framework. It acknowledges the specific financial pressures and priorities of a person.

By adjusting the traditional budgeting rules to better fit your personal and professional life, anyone can achieve a more balanced lifestyle.

The goal is to be prepared for the future while you’re able to enjoy the present.

Each budgeting method has its merits, and the best choice depends on individual financial situations and goals.

Don’t copy someone’s system. Instead, understand the concept behind, test it and build your own.

People might find it beneficial to start with a standard model like the 50-30-20 rule and adapt it over time to reflect their changing needs and priorities.

There is no correct or wrong approach. What exists are a personalized budget rules that suit your needs and evolve as you progress in life.

“Money never made a man happy yet, nor will it. The more a man has, the more he wants. Instead of filling a vacuum, it makes one.”

Benjamin Franklin

PS: I ask your prayers to Brazilian population. Severe floods devastated entire cities last weeks. If you can donate, please see details here. Thank you! 💛💚

Talk to you next week.

Light and peace,

—FMV

🧠 My Mental Download:

📕 (1) What I'm reading:

🎧 (2) What I'm listening to:

🤓 (3) What I'm studying:

🤿 Keep diving and exploring:

💡 Intellego is the process of gaining insights to better understand the world.

✍️ Letter is written by Fabíola Maia-Veres every Tuesday at 7pm.

🐝 Newsletter is configured and sent by BeeHiiv.

💬 📝 How did it go?

Any comments, critics, or suggestions? Reply to this email or reach out on Instagram or LinkedIn. Your feedback fuels my writing.