- Intellego Newsletter

- Posts

- Silent Thief

Do you know the effects of inflation on your budget?

🎼 📖 Read Intellego #022 by listening to:

Facts

Imagine you go to a fair every year and buy snacks for your kids. Last year, you could get a popcorn for $2, a soda for $1, and a cotton candy for $2, totaling $5.

This year, popcorn costs $2.50, soda costs $1.50, and cotton candy costs $2.50. Now, to buy all three, you need $6.50 instead of $5.

This example shows how inflation makes everything more expensive. Meaning, your money doesn’t buy as much as it used to.

In 10 years, if you just place your savings in a safe, checking account or under your mattress, you could lose 50% of everything you have today.

Your money depreciates. Yes, you read correctly. You'd lose half of your hard-earned money in a decade.

There is an invisible force governing the money system. Five years or decades of your life disappear out of thin air.

Can you recall how many hours did you work for this amount of money - now lost? How much effort, sweat, tears? I guess many...

In the past three years, did you notice any price change in essential products? Bread, milk, eggs, meat, toothpaste, body lotion, beverages, and tobacco? All these items are more expensive.

Or maybe the package of your favorite snack or soda downsized. Too bad, right? I believe you’ve heard of shrinkflation before.

Have you noticed your shopping cart is no longer full? Perhaps, you need more money to buy the same items you used to buy one or two years ago, right?

Yeah! Inflation steals money from you by shrinking your purchasing power. And you don’t even recognize it.

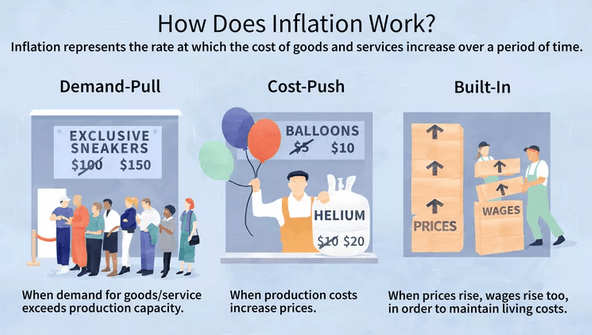

The Central Bank of every serious country operates under an inflation target regime. This goal could be 1%, 2%, 3%, 5%, 10% per year... it doesn't matter.

Here’s the truth. Central banks designed all fiat currency to lose buying power. They control the money supply.

If a central bank prints more money or lowers interest rates to stimulate the economy, it can lead to inflation. We’ve seen similar scenario after the pandemic. Increased money supply pushes prices up.

A sneaky mechanism to impoverish those who are just savers or live on a fixed-income. I know it's a bitter pill to swallow, but there is no sign that this will change in a near future. It is what it is.

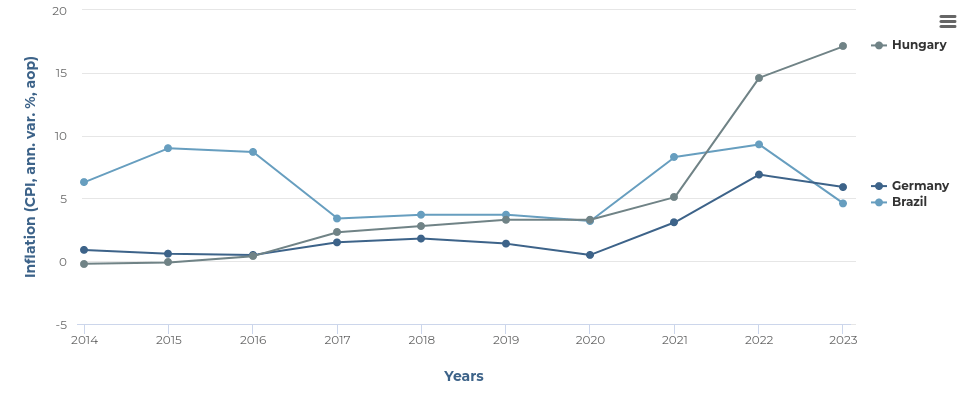

In developing countries, people lived or will experience episodes of hyperinflation because of political instability, currency devaluation, and economic mismanagement.

Dealing with 20%, 40%, 50%, 75%, 98% or even higher inflation rates became the norm for millions.

Imagine you receive your paycheck in the morning and you have to run to the groceries stores because prices increase daily.

My family went through this situation in the 80-90’s in Brazil. Hyperinflation has impacted and will keep impacting many families around the globe.

What are the biggest money lies we tell to ourselves? Figure out them sooner rather than later.

“Dealing with money it's less about spreadsheets and more about behaviors.”

Influences

If you live in Japan, the U.S., Eurozone or the UK, the financial landscape looks better. On average, if everything goes well, you will be 2-3% poorer this year alone. But we know things seldom go as expected.

And when it goes wrong, you can lose 10% or more of your purchasing power in a single year.

Inflation eats away your buying power. Your money loses value. Meaning, you can buy fewer goods and services with the same $10 bill compared to one year ago.

Let's illustrate with a real life example. Over the 30 years of the Real plan in Brazil, average inflation was 7.25% per year.

Let’s say you live in Brazil. This means that if you do nothing, your money will shrink by half in every 10 years.

You’d lose purchasing power if you don’t protect your savings wisely. Assuming you have saved some money, which is rare.

"Inflation takes from the ignorant and gives to the well informed”

Reasons

Why is money programmed to shrink?

But why does this occur? There is a consensus that a little inflation is healthy for an economy, as it would stimulate spending and investment.

And what can we do about this? Our money needs to at least keep up with inflation.

There is a minority of world’s population that saves money. The ones who do usually leave their money in a savings account with insane low interest rates.

As a result, your hard-earned money loses value to inflation. It disappears silently in months, years, decades. Hours of your life go down the drain.

Those who have some financial education even invest in other assets, aiming to get some real gain. Stocks, bonds, real state. Research, exercise your due diligence and name your heroes.

But then the government comes to subtract part of your profits via income tax. Not to mention the taxation of unrealized gains and tax on dividends. There's no free lunch in this world.

Is there any alternative? Yes! Become financially literate. Earn, plan, budget, save and invest. Move your money to where it’s treated best, preferably with zero or low management fees.

Learn money dynamics, and how to navigate the ever-changing world order.

Eliminate debt, have a budget, save and invest so that your assets grow at rates greater than inflation.

Acquiring knowledge and applying it enables you to reclaim time. Education is freedom. An asset no one can take from you.

"Inflation is as violent as a mugger, as frightening as an armed robber, and as deadly as a hit man."

Concepts

Source: Investopedia

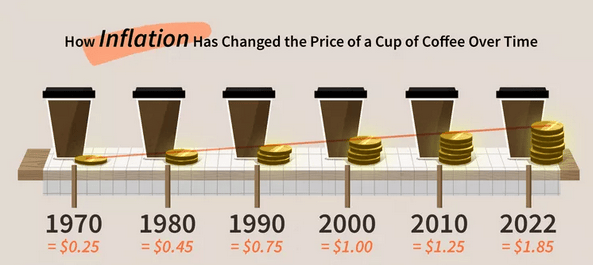

Purchasing power measures what a unit of currency can buy, while inflation measures rising prices. Let me give you two examples to make this clear.

Example 1: Let's say a movie ticket cost $5 last year. This year, you go to buy a ticket and it costs $6. The price has gone up $1 because of inflation.

You can say: "It was only $1 increase. It's nothing." Now, imagine this price increase in every single product or service you purchase in a month or year.

From petrol to medicines. From clothes to concert tickets. Don't you think it would matter? I certainly think so.

Example 2: Last summer, you had $10, and you could buy 5 ice creams because each ice cream cost $2. This summer, you still have $10, but now each ice cream costs $2.50.

Now you can only buy 4 ice creams with the same $10. Your purchasing power has decreased because your $10 doesn't go as far as it used to.

To sum up, example 1 refers to the concept of inflation - the overall increase in prices. While example 2 relates to purchasing power - the amount of goods or services that one unit of money can buy.

Concepts inversely correlated. Inflation diminishes our purchasing power. As prices rise, the quantity of goods or services we can afford with a certain amount of money decreases.

“Inflation destroys savings, impedes planning, and discourages investment. That means less productivity and a lower standard of living.”

Impacts

Source: Investopedia

Inflation impacts our daily life. It affects families and economies in various ways:

Reduced purchasing power: Inflation diminishes the value of money, meaning families can buy less with the same amount of currency.

Savings and investments: High inflation can erode the real value of savings and reduce the real rate of return on investments.

Fixed-income households: Retirees and families on fixed incomes may struggle as their income shrinks with inflation, leading to financial strain.

Paying off debt: Inflation can have a mixed impact on debt. While it may reduce the real value of fixed-rate debt over time, it can also increase the cost of variable-rate loans.

Cost of living: Everyday expenses such as groceries, utilities, and rent may rise, putting additional pressure on family budgets.

Long-term planning: Inflation can make it challenging for families to plan for long-term goals like education, retirement, or buying a home.

"Inflation is taxation without legislation."

Conclusion

From daily expenses to long-term financial goals. Inflation can significantly affect families’ financial health. And it can be quite challenging for those on fixed incomes or with significant variable-rate debts.

We cannot deny the negative impact of inflation. It takes more money from our pockets. It erodes the value of money, affecting economies and people globally.

By understanding the causes and impacts of inflation, we can better prepare for its effects on our finances. We can make informed decisions to protect and grow our wealth.

Inflation is a natural part of economic cycles. Managing it effectively is crucial to maintaining financial stability and ensuring a fair standard of living for you and your family.

“If you live according to nature; you will never be poor. If you live according to the world's caprice, you will never be rich.”

Talk to you next week.

Light and peace,

—FMV

🧠 My Mental Download:

📕 (1) What I'm reading:

🎧 (2) What I'm listening to:

📺 (3) What I'm re-watching:

🤿 Keep diving and exploring:

💡 Intellego is the process of gaining insights to better understand the world.

✍️ Letter is written by Fabíola Maia-Veres every Tuesday at 7pm.

🐝 Newsletter is configured and sent by BeeHiiv.

💬 📝 How did it go?

Any comments, critics, or suggestions? Reply to this email or reach out on Instagram or LinkedIn. Your feedback fuels my writing.